The Current Landscape of Financial Inclusion in Emerging Markets

Emerging markets, often characterized by rapid economic growth and evolving infrastructure, present a unique blend of financial systems. These systems typically consist of both traditional financial institutions like banks and microfinance organizations, as well as innovative non-traditional services such as mobile money platforms.

Common features of these financial systems include

- Limited access to formal banking: Many people in these regions lack access to banking services, relying on informal financial practices.

- Predominance of cash transactions: Cash remains the main payment method, challenging efforts to build a digital or cashless economy.

- High costs of financial services: Transaction fees, interest rates, and other costs are often high, especially for low-income individuals.

- Regulatory hurdles: Outdated or inconsistent regulations hinder innovation and slow the growth of financial markets, making financial inclusion difficult.

Key Barriers to Financial Inclusion

Several challenges contribute to the exclusion of many from the formal financial ecosystem in emerging markets:

- Geographical limitations: Remote areas frequently suffer from a lack of financial infrastructure, limiting access to services like banking or ATMs.

- Low financial literacy: Many individuals lack the knowledge required to navigate financial products or services effectively.

- High transaction costs: The costs associated with accessing financial services can be prohibitive, especially for low-income populations.

- Identity verification issues: Many people may not possess the required documentation to open a bank account, making formal financial participation impossible.

- Technology gaps: A lack of smartphones or reliable internet connectivity in underserved areas limits the adoption of digital financial services.

To combat these issues, a growing number of governments, financial institutions, and development organizations are promoting solutions like financial education, expanding digital payment systems, and fostering the growth of microfinance institutions. These efforts are paving the way for a more inclusive financial landscape in emerging markets.

How Blockchain and AI Are Shaping the Future of Financial Inclusion

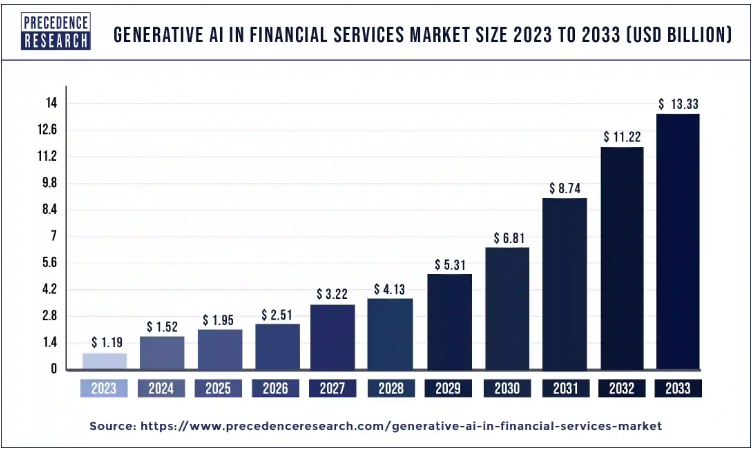

The combined power of blockchain and artificial intelligence (AI) holds immense potential to revolutionize financial inclusion, particularly in underserved regions. Together, these technologies can address longstanding challenges related to identity verification, credit access, and transaction transparency. Global Artificial Intelligence (AI) in Banking, Financial Services, and Insurance (BFSI) Market size was valued at USD 20.15 Billion in 2022 and is poised to grow from USD 26.24 Billion in 2023 to USD 246.04 Billion by 2031, growing at a CAGR of 32.5% in the forecast period (2024-2031).

SOURCE

Blockchain’s Impact on Digital Identity

One of the primary barriers to financial inclusion in emerging markets is the absence of secure and verifiable digital identities. Many individuals lack official documentation, making it difficult to access formal financial services. Blockchain offers a decentralized, tamper-proof solution for storing and verifying digital identities.

Key advantages of blockchain-based digital identity systems include:

- Enhanced data security: Blockchain’s decentralized structure and cryptographic techniques make it extremely challenging for unauthorized parties to alter or steal sensitive personal information.

- Empowerment and control: Individuals can manage their digital identities independently, without needing intermediaries like banks or government institutions.

- Cross-platform compatibility: Blockchain enables the creation of identities that can be recognized and used across multiple platforms, eliminating the need for redundant verification processes.

AI-Driven Credit Scoring and Risk Assessment

Conventional credit scoring models often exclude those without formal credit histories, leaving many individuals in emerging markets underserved. AI offers an alternative by incorporating diverse data sources—such as utility bills, mobile phone usage, and even social media behavior—to build more comprehensive credit profiles.

Key benefits of AI-based credit scoring models include:

- Increased accuracy: AI algorithms can analyze vast datasets to detect correlations and patterns that human analysts may overlook, leading to more precise risk assessments.

- Greater inclusivity: By factoring in non-traditional data points, AI models can expand financial services to previously overlooked individuals.

- Bias mitigation: With the right design, AI can reduce biases inherent in traditional credit scoring systems, promoting fairness in financial access.

Smart Contracts for Trust and Efficiency

Smart contracts, which are self-executing agreements stored on a blockchain, provide transparency and automation in financial transactions. These digital contracts can facilitate various financial services, from peer-to-peer lending to remittances and insurance, without the need for intermediaries.

Notable advantages of smart contracts include:

- Transparency and trust: Smart contracts are publicly verifiable on the blockchain, ensuring that all parties can see the terms and conditions.

- Operational efficiency: Automating financial processes through smart contracts reduces administrative costs and accelerates transaction times.

- Security and reliability: Blockchain ensures that smart contracts are immutable and can only be triggered when pre-defined conditions are met, minimizing fraud risks.

By integrating blockchain for secure identity verification and AI for inclusive credit scoring, financial institutions can build more accessible systems. These technologies offer a pathway to providing millions in emerging markets with much-needed financial tools, fostering economic empowerment and financial resilience.

The Expanding Role of AI in Financial Services Access

Artificial intelligence (AI) is playing a transformative role in expanding access to financial services, particularly in emerging markets. By automating processes, improving risk assessment, and offering personalized financial experiences, AI has the potential to reshape the financial landscape for underserved populations.

AI-Driven Enhancements in Microcredit and Microlending

Microcredit and microlending have become critical tools for empowering individuals and small businesses in regions with limited access to traditional financial services. AI is revolutionizing these programs by:

- Advancing credit scoring models: AI uses alternative data like mobile phone usage, utility payments, and social media activity to assess creditworthiness more accurately, even for those with limited credit history.

- Automating loan processes: AI streamlines loan applications, automates approvals, and reduces the time it takes for borrowers to access funds.

- Delivering personalized financial education: It offer tailored advice on budgeting, saving, and loan repayment, empowering borrowers to make informed financial decisions.

Personalization of Financial Services Through AI

AI’s ability to analyze vast amounts of customer data enables financial institutions to tailor services to individual needs, offering a more personalized experience. Key ways AI is achieving this include:

- Customizing product offerings: AI analyzes customer preferences and behaviors to recommend products aligned with financial goals, boosting satisfaction.

- Providing personalized financial advice: AI tools like virtual advisors and chatbots offer tailored recommendations, helping customers make informed decisions.

- Enhancing customer experience: AI automates tasks like account inquiries and transaction processing, delivering faster and more efficient service.

AI for Smarter Credit Scoring in Emerging Markets

Traditional credit scoring systems often fall short in emerging markets, where formal financial infrastructure may be limited. These systems typically rely on data like credit history and income, excluding large populations who lack access to formal credit. In such regions, many individuals have limited or no credit history, leaving them underserved and unable to access essential financial services.

AI-based credit scoring systems, however, offer a game-changing alternative. They can process a far more extensive range of data, including non-traditional sources like online behavior, and even mobile phone usage. By doing so, AI can create more accurate and inclusive credit scoring models that provide access to credit for millions.

Utilizing Non-traditional Data to Assess Creditworthiness

One of the most significant advantages of AI-driven credit scoring is its ability to draw from unconventional data sources. This opens up entirely new ways to assess creditworthiness:

- Alternative credit data: AI can analyze recurring payments, like utility bills and rent, to provide a clearer view of a person’s financial reliability.

- Social media data: AI systems can review social media activity to gain insights into spending habits, lifestyle, and risk profiles.

- Online behavior data: Data from online purchases and browsing habits help AI assess financial behavior and credit risk.

- Mobile phone usage: In emerging markets, mobile phone data—such as call history and location patterns—can be valuable for evaluating creditworthiness, especially when other financial data is lacking.

Success Stories of AI-Powered Credit Scoring

AI-powered credit scoring is already making a tangible impact in emerging markets, with several success stories illustrating its potential:

- Lendable (Philippines) uses AI to assess creditworthiness through alternative data points like mobile phone usage and social media activity. This approach has helped millions of Filipinos access loans, many for the first time, promoting financial inclusion nationwide.

- KreditBee in India leverages AI to analyze various data sources, including online purchases and mobile phone usage. This enables the company to provide credit to millions of Indians who have little or no formal credit history. This innovation has significantly widened access to financial services, boosting economic growth and improving livelihoods.

{kind=link}